The Chiropractic Conundrum: Is It Covered by Your Medical Insurance?

Why Understanding Chiropractic Insurance Coverage Matters

Does medical insurance cover chiropractic care? The short answer is: it depends on your specific plan, but most insurance types provide some level of coverage.

Quick Coverage Overview:

– Private Insurance: Most PPO and HMO plans cover chiropractic with copays ranging from $10-$40

– Medicare: Covers manual spinal manipulation for subluxation (you pay 20% after deductible)

– Medicaid: Coverage varies by state – some cover it, others don’t

– Employer Plans: Usually included with visit limits of 10-30 sessions per year

– Workers’ Comp/Auto: Typically covers accident-related chiropractic care

More than 35 million Americans visit chiropractors each year. As chiropractic care becomes more mainstream for treating back pain, headaches, and musculoskeletal issues, understanding your insurance coverage becomes crucial.

Coverage rules vary wildly between insurers. Some plans require referrals, others limit you to specific networks or cap your visits. Most importantly, many plans only cover “medically necessary” active treatment – not ongoing maintenance care.

With chiropractic sessions typically costing $30-$200 per visit, knowing what your insurance covers can save you hundreds or thousands of dollars.

Does Medical Insurance Cover Chiropractic Care?

The answer to “does medical insurance cover chiropractic” care isn’t a simple yes or no – it depends on several important factors.

Most health insurance plans do provide some level of chiropractic coverage. However, it’s typically classified as an ancillary benefit rather than an essential health service under the Affordable Care Act, meaning details vary between plans and insurers.

Medical Necessity Makes All the Difference

Insurance companies will only cover chiropractic care when it’s deemed “medically necessary” – meaning you’re receiving active treatment for a specific health condition rather than general wellness care.

This typically covers spinal manipulation to correct vertebral subluxations, acute back and neck pain, post-injury rehabilitation, and management of chronic conditions with documented improvement. Scientific research on spinal manipulation supports the effectiveness of these treatments.

The key distinction is between active treatment (initial phase after injury or during acute pain with expected measurable improvement) and maintenance care (routine visits once condition stabilizes).

Understanding Your Visit Limits

Most plans cap chiropractic visits at 10 to 30 sessions annually. Some plans also set monthly limits or require periodic reviews. These caps typically reset on January 1st.

The Referral Question

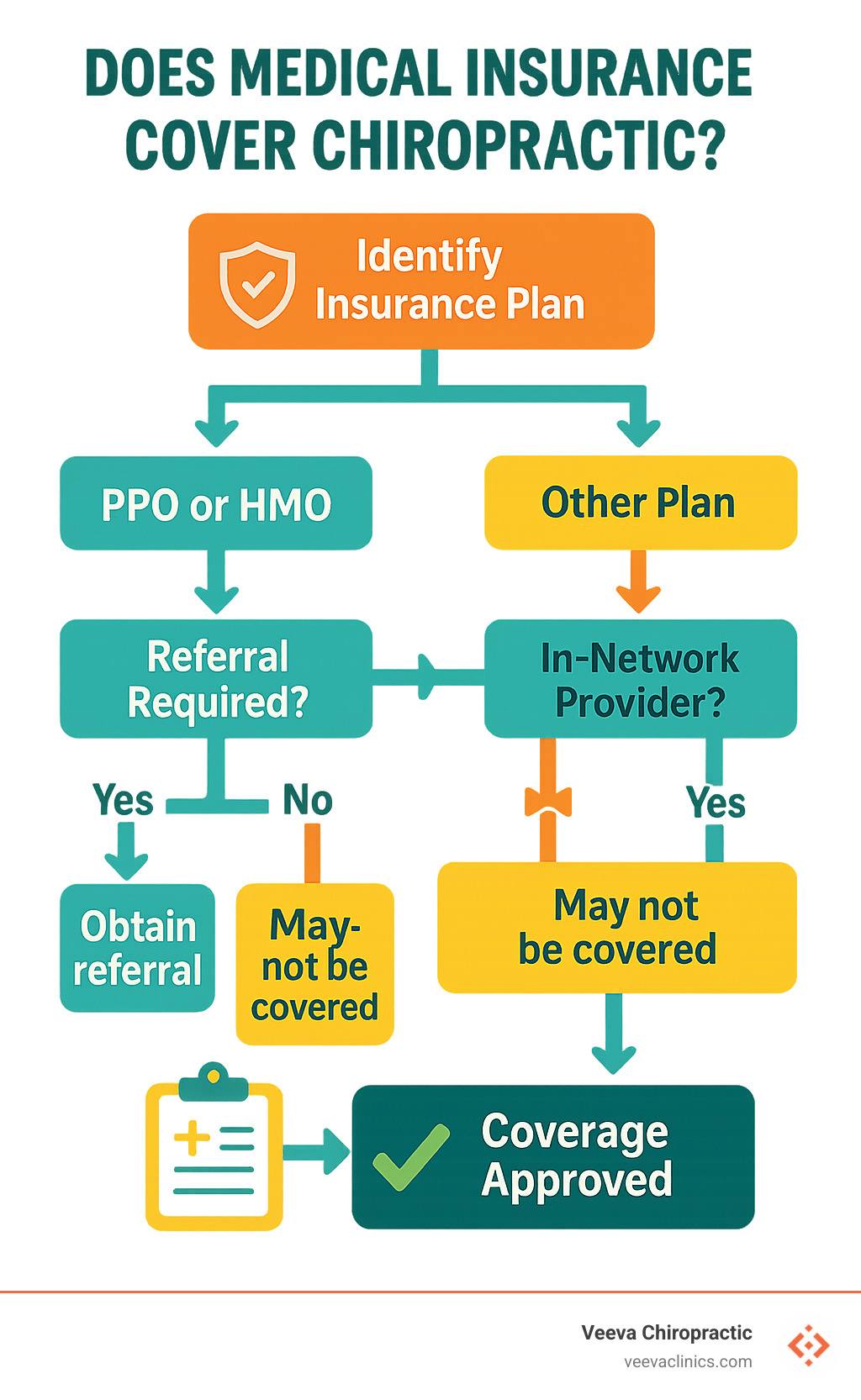

HMO plans almost always require referrals, while PPO plans usually allow direct access to in-network chiropractors.

How Your Deductible Affects Things

If you haven’t hit your annual deductible, you’ll pay full cost until you do. Once you’ve met that threshold, you’ll typically pay either a copay or percentage of the cost.

How does medical insurance cover chiropractic under different plan types?

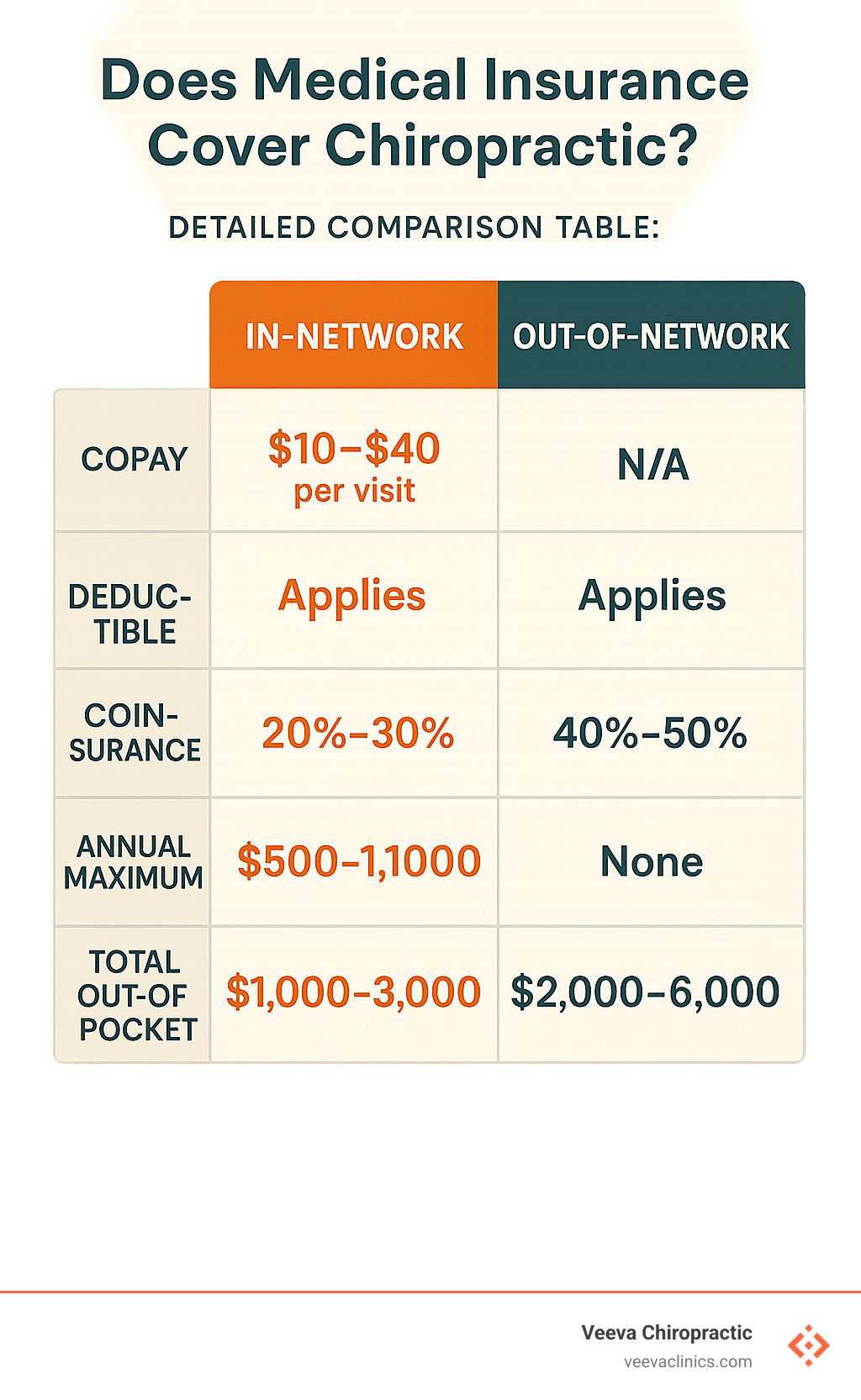

Private PPO plans offer the most flexibility. You can see in-network chiropractors with lower copays (typically $15 to $30 per visit) or go out-of-network for higher costs. No referral requirements, though you might face higher deductibles.

HMO plans require staying within their network and usually need primary care physician referrals first. Trade-off is often lower copays ($10 to $20 per visit) once you have proper authorization.

Employer group plans often include chiropractic benefits as wellness programs, frequently more generous than individual policies with up to 20 to 30 visits annually.

Medicare Part B covers manual spinal manipulation by enrolled chiropractors for treating vertebral subluxations. You pay 20% of Medicare-approved amount after meeting your Part B deductible. Medicare won’t cover X-rays ordered by chiropractors.

Medicaid coverage varies dramatically by state since chiropractic is considered optional. Some provide comprehensive coverage while others offer none.

Workers’ compensation and auto Personal Injury Protection (PIP) typically provide full coverage for accident-related chiropractic care with no copays or deductibles.

Does medical insurance cover chiropractic for maintenance care?

Insurance companies draw a clear line between active treatment (covered) and maintenance care (typically not covered). Once your condition reaches a “treatment plateau” without measurable improvement, visits get reclassified as maintenance.

Maintenance care includes routine adjustments for general wellness, preventive visits, ongoing treatment without documented progress, and care primarily for comfort rather than correction.

Proving Active Treatment

To maintain coverage, your chiropractor must document continued progress through objective pain measurements, improved range of motion, functional capacity evaluations, and documented symptom reduction.

When Coverage Gets Denied

If your insurer denies coverage, you can request peer-to-peer review, provide additional documentation, have your primary care physician write supporting letters, or file formal appeals with clinical evidence.

At our Oregon clinics, we work closely with patients to document progress and steer coverage challenges, especially for auto accident and workplace injuries where continued improvement is often measurable.

Breaking Down Coverage by Insurance Type

Each insurance type has its own approach to chiropractic coverage – some generous, others restrictive.

The Private Insurance Landscape

Private insurance plans generally include chiropractic coverage, but since the Affordable Care Act doesn’t consider it essential, insurance companies have flexibility in coverage levels.

Most private plans cover 10-30 chiropractic visits annually, resetting each January. Coverage generosity often correlates with premium costs.

ACA Marketplace Plans

Some states require marketplace plans to cover chiropractic care, while others make it optional. Plans with chiropractic benefits might cost $50 more monthly but can save hundreds in out-of-pocket costs.

Medicare: Simple but Limited

Medicare Part B covers manual spinal manipulation for correcting vertebral subluxations. They won’t cover X-rays ordered by chiropractors, massage therapy, or maintenance care.

Medicaid: State-Dependent

Since chiropractic is optional under Medicaid, coverage depends entirely on your state. Even covering states often impose strict visit limits and smaller provider networks.

Employer Plans: Often the Best Deal

Large employers frequently self-fund health plans, giving them freedom to design comprehensive benefits. Many recognize that covering chiropractic care prevents more expensive medical problems. Scientific research on chronic back pain supports this preventive approach.

Private & Employer-Sponsored Plans

Network Choices Matter

In-network providers offer lower copays (usually $15-$40 per visit) and no surprise bills. Out-of-network providers can charge whatever they want, leaving you to pay the difference.

Understanding Cost Structure

Some plans charge flat copays for each visit. Others use coinsurance where you pay a percentage of total cost. Copays are more predictable; coinsurance varies based on provider fees.

Pre-Authorization Requirements

Some plans require pre-authorization for chiropractic care, especially for extended treatment. Most chiropractic offices handle this paperwork for you.

High-Deductible Plans and Tax-Advantaged Accounts

High-deductible plans require paying full price until meeting your deductible, but often pair with HSAs or FSAs that let you pay with pre-tax dollars.

Medicare & Medigap

The Subluxation Requirement

Medicare Part B only covers chiropractic care for treating vertebral subluxations – spinal bones out of normal position that can be corrected through manual manipulation.

Your Cost Sharing

After meeting Medicare Part B deductible, you pay 20% of Medicare-approved amount – typically $15-$25 per visit.

No Visit Limits

Medicare doesn’t limit sessions as long as each visit is medically necessary for treating subluxation.

Medicare Advantage: Extra Benefits

Medicare Advantage plans often provide additional chiropractic benefits beyond original Medicare, including coverage for X-rays, expanded treatments, or lower copays.

More info about costs after accidents helps Medicare beneficiaries understand accident-related coverage.

Medigap: Filling the Gaps

Medigap policies can cover that 20% coinsurance for chiropractic services, potentially reducing out-of-pocket costs to zero.

Medicaid & State Mandates

Medicaid chiropractic coverage depends entirely on your state since it’s an optional benefit.

States covering chiropractic often impose limited annual visits (12-20), prior authorization requirements, restricted provider networks, or age limitations.

Some states differentiate between pediatric and adult coverage, with different rules for each population.

Medicaid programs typically require extensive documentation including treatment plans, progress reports, and medical necessity justifications.

In Oregon, where our clinics operate, Medicaid provides some chiropractic coverage with limitations on visit frequency and provider networks.

Costs, Limitations, and Out-of-Pocket Strategies

Even when insurance covers chiropractic care, you’ll likely have some out-of-pocket costs. Understanding these expenses helps you budget wisely.

What You Can Expect to Pay

First visits typically cost $60-$200 (includes consultation, examination, treatment). Regular adjustments range from $30-$65. Comprehensive treatment sessions with additional therapies cost $75-$150.

Your Insurance Copay Reality

HMO plans typically offer $10-$20 copays, PPO plans charge $15-$30. High-deductible plans require full payment until deductible is met, then 20-30% coinsurance.

The Visit Limit Challenge

Basic plans: 6-12 visits annually

Standard plans: 12-20 visits annually

Premium plans: 20-30 visits or unlimited if medically necessary

Smart Money Moves with HSAs and FSAs

These accounts let you pay with pre-tax dollars, saving 22-37% depending on your tax bracket.

Cash-Pay Advantages

Many chiropractors offer 10-25% discounts for cash-paying patients, plus package deals or sliding scale fees.

Navigating In-Network vs Out-of-Network Providers

Choosing in-network versus out-of-network chiropractors can save or cost you hundreds of dollars.

Finding the Right Provider

Verify network status before booking appointments. Check your insurance company’s online directory and call member services to confirm. Also verify with the chiropractor’s office that they accept your specific plan.

Making Out-of-Network Work

You might get partial coverage through superbill reimbursement – pay upfront, get detailed receipt, submit to insurance for 50-70% reimbursement of their “allowed amount.”

The Balance Billing Reality

Out-of-network providers can charge you the difference between their fee and insurance payment. If chiropractor charges $100, insurance pays $60, you owe $40 plus deductible/coinsurance.

Negotiation Tips

Discuss costs upfront. Many providers offer payment plans or cash-pay discounts. Some might accept insurance payment as full payment.

Is Chiropractic Care Covered by Insurance After a Car Accident? provides accident-specific coverage guidance.

What To Do If Your Plan Excludes Chiropractic

Appeals Process

If claims get denied, request detailed explanation of denial reason. Gather supporting documentation and ask your primary care doctor for a physician support letter explaining medical necessity.

Submit formal appeal with medical evidence. Many insurers offer peer-to-peer reviews where your chiropractor speaks directly with their medical director.

Alternative Solutions

Consider specialized chiropractic discount plans or supplemental insurance. Look into chiropractic college clinics with supervised students providing reduced-rate care.

Most chiropractic offices offer interest-free payment plans or income-based sliding fees.

At our Beaverton, Happy Valley, Hillsboro, and Gresham locations, we work with patients to find affordable solutions, especially for auto accident and workplace injuries.

Maximizing Your Benefits & Next Steps

Getting the most from your chiropractic insurance benefits requires planning and preparation.

Start with benefit verification – call your insurance company before your first appointment. Ask about copay amounts, deductible status, available visits, and referral requirements.

If referrals are required, clearly describe symptoms to your primary care physician and request referrals with “medical necessity” language and sufficient visits.

Document your progress throughout treatment. Your chiropractor will track pain levels, range of motion, and daily function improvements – this documentation protects your coverage.

Consider combining care types if your plan covers both physical therapy and chiropractic, effectively doubling available visits.

Timing matters for deductibles and annual limits. Plan intensive treatment when it’s most cost-effective.

Using HSAs and FSAs Efficiently

Pre-tax advantages are substantial – every $100 in an HSA/FSA costs only about $78 in take-home pay for someone in the 22% tax bracket.

Some administrators require Letters of Medical Necessity for chiropractic expenses, which your chiropractor can easily provide.

Understanding rollover rules: HSAs roll over indefinitely and can be invested; FSAs typically follow “use it or lose it” rules with small carryovers.

Keep detailed records of all chiropractic expenses including receipts and service documentation.

Leveraging Auto & Work-Injury Policies

Accident and work injury coverage is often much more generous than regular health insurance.

Personal Injury Protection (PIP) in no-fault states covers chiropractic care immediately after auto accidents without copays, deductibles, or fault determination.

Workers’ compensation provides comprehensive chiropractic benefits with no cost-sharing for approved job-related injuries.

Coordinating multiple policies can maximize benefits – work with providers to determine optimal billing order.

At our clinics in Beaverton, Happy Valley, Hillsboro, and Gresham, we handle complex insurance scenarios daily, especially for auto accident and workplace injuries. More info about accident coverage explains how different coverage types work together.

Frequently Asked Questions about Chiropractic Insurance Coverage

1. Do I need a referral for insurance to pay for chiropractic visits?

Referral requirements depend on your plan type:

HMO Plans almost always require referrals from your primary care physician. You need to schedule with your PCP first, explain symptoms, request referral specifying visits and duration, then stay within referral parameters.

PPO Plans typically allow direct access to in-network chiropractors without referrals, though some may require referrals for extended treatment.

Medicare doesn’t require referrals for chiropractic care treating documented vertebral subluxation.

Medicaid requirements vary by state.

Even when not required, having a referral can strengthen your case for medical necessity.

2. How many chiropractic sessions are usually covered each year?

Typical Coverage Limits:

– Basic plans: 6-12 visits per year

– Standard employer plans: 12-20 visits per year

– Premium plans: 20-30 visits per year

– Medicare: Unlimited if medically necessary for subluxation

– Workers’ compensation: No preset limits for approved injuries

– Auto PIP: Varies by state and policy

Limits typically reset January 1st. Some plans have monthly limits in addition to annual caps.

3. Are ancillary services like massage or acupuncture included in my benefits?

Commonly Covered Services:

– Spinal manipulation and adjustments

– Initial examinations and consultations

– Some therapeutic modalities (ultrasound, electrical stimulation)

– Exercise therapy and rehabilitation

Services Often NOT Covered:

– Massage therapy (unless specifically prescribed and included)

– Acupuncture (except Medicare covers it for chronic lower back pain in limited circumstances)

– Nutritional counseling

– X-rays ordered by chiropractors (Medicare excludes these)

– Maintenance or wellness care

Verify coverage by reviewing your plan’s Summary of Benefits, calling member services, and requesting written confirmation for expensive treatments.

At our clinics, we provide comprehensive services and help patients understand coverage while exploring payment options for uncovered treatments.

Conclusion

Understanding does medical insurance cover chiropractic care becomes simpler once you know what questions to ask. Most insurance plans do provide some coverage – you just need to understand how to work within their rules.

Most insurance plans will cover your chiropractic care when it’s medically necessary, but they exclude maintenance visits focused on feeling good rather than getting better.

Coverage varies significantly by plan type – PPOs offer more freedom, HMOs need referrals, Medicare focuses on specific spinal conditions, and Medicaid depends on your state. Know your plan’s requirements and work with them.

Staying in-network saves serious money, timing treatments strategically around deductibles helps, and using HSA/FSA accounts provides pre-tax savings.

When accidents happen, auto insurance and workers’ compensation typically provide comprehensive coverage without usual health insurance restrictions.

Your action plan starts with one phone call to your insurance company’s member services. Ask about chiropractic benefits, visit limits, copays, and referral requirements before you need care.

If your plan denies coverage, don’t give up. Appeals work when you provide proper documentation and physician support for medical necessity.

At Veeva Chiropractic, we’ve helped thousands of patients in Beaverton, Happy Valley, Hillsboro, and Gresham steer insurance complexities. We handle paperwork so you can focus on feeling better. Whether dealing with auto accidents, workplace injuries, or chronic pain, we work with your insurance to maximize benefits.

Don’t let insurance confusion keep you from getting needed care. With the right information and a healthcare partner who understands the system, you can access effective chiropractic treatment while keeping costs manageable.

More info about chiropractic coverage in Oregon provides additional state-specific guidance for maximizing your benefits.