Navigating Insurance: Ensuring Your Chiropractic Care is Covered

Why Getting Insurance to Cover Your Chiropractic Care Matters

How to get insurance to pay for chiropractic care starts with understanding your benefits and following the right steps to file claims. Here’s what you need to know:

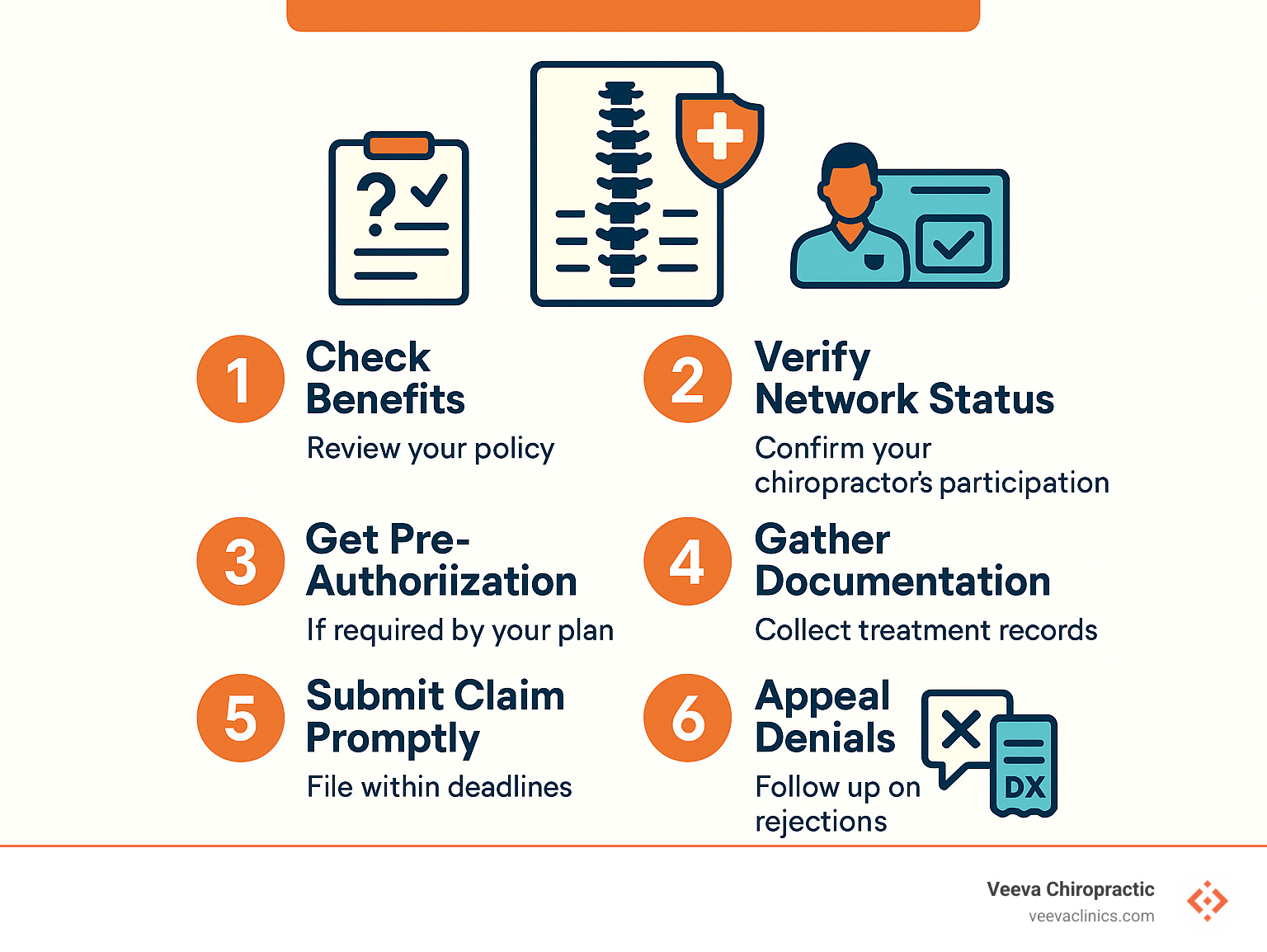

Quick Steps to Get Coverage:

1. Check your benefits – Review your policy for chiropractic coverage limits and requirements

2. Verify network status – Confirm your chiropractor accepts your insurance plan

3. Get pre-authorization if required by your plan

4. Gather documentation – Collect treatment notes, receipts, and diagnostic codes

5. Submit claims promptly – File within your insurer’s deadlines

6. Appeal denials – Follow up on rejected claims with additional evidence

Nearly 70% of Canadians have extended health care coverage that often includes chiropractic services, yet many people don’t know how to access these benefits. In Ontario alone, 4 out of 5 chiropractic patients pay for their care through private insurance coverage.

Chiropractic care isn’t covered under provincial health plans like OHIP, but most workplace benefits and private insurance plans do provide coverage. Understanding how to steer this system can save you hundreds of dollars each year on treatments for back pain, neck stiffness, and other musculoskeletal issues.

Most extended health plans reimburse $20 to $50 per chiropractic visit, up to annual limits of $500 to $1,000.

Important how to get insurance to pay for chiropractic care terms:

– does insurance cover chiropractic care

– does insurance cover wellness or maintenance chiropractic care

How to Get Insurance to Pay for Chiropractic Care: Step-By-Step Blueprint

How to get insurance to pay for chiropractic care becomes much simpler when you know the right steps to take. At Veeva Chiropractic, we’ve helped thousands of patients across our Beaverton, Happy Valley, Hillsboro, and Gresham locations turn their insurance benefits into real savings.

The secret isn’t complicated—it’s all about being prepared and knowing what your insurer expects from you.

Your insurance success starts with understanding key terms. When you call your insurer, ask about your eligibility for chiropractic services and whether your provider is a network provider. You’ll also need to know your deductible amount and how it applies to paramedical care.

Direct billing can be a game-changer if your chiropractor offers it. This means we submit the claim directly to your insurance company, and you only pay the difference. If direct billing isn’t available, you’ll need to handle the superbill—that’s the detailed receipt with all the medical codes your insurer needs.

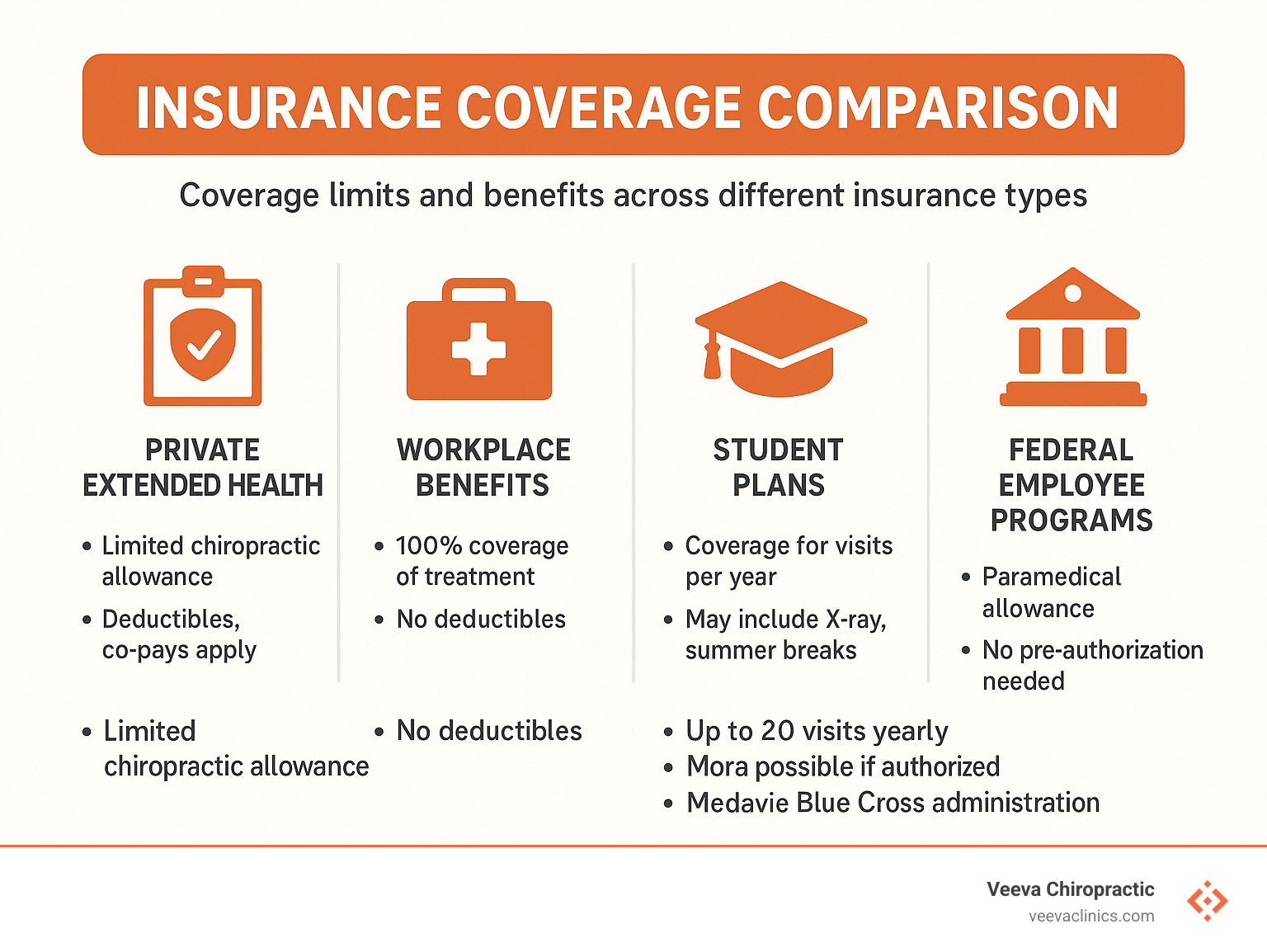

| Coverage Type | Typical Benefits | Common Limitations |

|---|---|---|

| Private Extended Health | $20-$50 per visit, up to $500-$1,000 annually | 10-30 visits per year, referral may be required |

| Workplace Benefits | Similar to private plans, often more generous | Varies by employer plan |

| Auto Insurance (PIP) | Full coverage for accident-related injuries | Must be accident-related, time limits apply |

| Workers’ Compensation | Full coverage for work injuries | Must be work-related, requires employer reporting |

Confirm Your Benefits Before the First Visit

Spending fifteen minutes reviewing your policy booklet or logging into your benefits portal can save you from sticker shock later.

Start by looking for “paramedical services” or “alternative therapies.” Chiropractic care usually falls under the paramedical category along with massage therapy and physiotherapy.

Your benefits portal should tell you everything you need to know. Look for your annual maximum—that’s the total dollar amount your plan will cover for chiropractic care each year. Also check your co-payment amount, which is what you’ll pay out-of-pocket for each visit.

If you’re still confused after reviewing your documents, call your insurance company directly. Have your member ID ready and ask specific questions. Get the exact dollar amounts, visit limits, and any special requirements.

Steer Pre-Authorizations & Referrals to Ensure Insurer Payment

Some insurance plans want to approve your treatment before you start, while others are happy to pay after the fact.

Here’s what makes Oregon special: Chiropractors have primary care status in our state, which means you typically don’t need a referral from your family doctor. However, your specific insurance plan might still have its own referral rules.

Pre-authorization is your insurance company’s way of saying “yes, we agree this treatment makes sense” before you start care. Not all plans require it, but when they do, getting approval upfront prevents headaches later.

You’ll typically need pre-approval if your plan explicitly requires it, you’re planning extensive treatment, or you need specialized services beyond basic adjustments.

For more detailed information about coverage requirements in our state, check out Is Chiropractic Care Covered by Insurance in Oregon State? which explains the specific rules that apply to Oregon residents.

Meeting the Paperwork Requirements That Open up Reimbursement

Insurance companies speak one language fluently: paperwork. Once you know what they’re looking for, getting your chiropractic care covered becomes much more predictable.

Every successful insurance claim needs the same basic ingredients. Claim forms either come from you or your chiropractor’s office. CPT codes are the specific numbers that tell your insurer exactly what treatment you received. ICD-10 codes explain the medical reason you needed treatment.

Your treatment plan shows your insurer this isn’t just random care—there’s a clear goal and expected timeline. Receipt standards require detailed invoices showing dates, services, and provider information.

At Veeva Chiropractic, we handle the complex coding and can submit claims directly to your insurer in many cases.

Gather the Right Documentation Every Time You See Your Chiropractor

Documentation is what turns a legitimate treatment into a successful insurance claim. Without proper records, even the most necessary care can get denied.

Progress notes form the backbone of your claim. These detailed records from each visit show your symptoms, the treatment you received, and how you responded.

Objective measures give insurance companies the concrete data they love. Things like range of motion tests, pain scale ratings, and functional assessments prove your treatment is working. Imaging reports from X-rays or MRIs provide additional medical evidence when relevant.

At Veeva Chiropractic, we maintain comprehensive electronic health records that make insurance submissions much smoother. Every visit gets documented with objective measures and progress tracking—exactly what insurers need to approve claims.

Scientific research on manual therapy cost-effectiveness shows that well-documented chiropractic care actually reduces overall healthcare costs.

Submit the Claim (or Let Your Clinic Do It for You)

This is where your preparation pays off—actually getting your claim to the insurance company.

Direct billing is hands-down the easiest option for patients. Many chiropractic clinics, including all Veeva Chiropractic locations, can bill your insurance directly. You pay any co-payment or deductible upfront, and we handle all the submission details.

Electronic claims through insurer apps have become surprisingly user-friendly. Most major insurance companies now offer smartphone apps where you can photograph receipts and submit claims instantly.

Traditional mail submission still works perfectly fine, though it takes longer to process. If you go this route, always make copies of everything before mailing.

Timing matters more than you might think. Most insurers require claims within 12 months of receiving treatment, but some plans have stricter deadlines. Auto insurance claims often have even tighter timeframes.

Claim deadlines aren’t suggestions—they’re hard rules. Miss the deadline, and even the most legitimate claim gets denied automatically.

Maximizing Benefits & Avoiding Surprise Bills

Getting the most out of your chiropractic benefits is like being a savvy shopper—you want to stretch every dollar while avoiding unpleasant surprises.

Most insurance benefits reset on January 1st, but some plans follow your employer’s fiscal year instead. Knowing your exact reset date can be a game-changer for planning your care.

Understanding visit caps helps you avoid that awkward moment when your insurance won’t cover today’s visit. Most plans limit chiropractic visits to somewhere between 10 and 30 per year.

Here’s a strategy that works beautifully for couples: multi-plan coordination. If both you and your spouse have benefits through work, you might be able to submit claims to your spouse’s insurer after using up your own coverage.

Don’t overlook your Health Savings Account or Flexible Spending Account. These let you pay for chiropractic care with pre-tax dollars, which can save you 20-30% even when insurance doesn’t cover everything.

Appeal or Re-File When a Claim Is Denied

Claim denials aren’t the end of the world, even though they feel that way. Insurance companies deny claims for all sorts of reasons, many of which have nothing to do with whether you actually needed treatment.

The most common culprit? Paperwork hiccups. Maybe a diagnostic code got transposed, or the claim was submitted after some deadline. Sometimes the insurance company’s computer system just has a bad day.

Start by carefully reading your Explanation of Benefits. Buried in there is the actual reason for denial. Look for phrases like “missing information,” “out-of-network provider,” or “exceeds plan limits.”

Your appeal doesn’t have to be a legal brief—just a clear explanation of why the claim should be paid. If the denial was for medical necessity, Scientific research on low back problems provides strong evidence supporting chiropractic care effectiveness.

Most insurers give you 30 to 60 days to appeal, so don’t procrastinate. The appeals process is usually straightforward: fill out their form, attach any additional documentation, and submit it.

At Veeva Chiropractic, we’ve helped countless patients successfully appeal denials. One patient’s claim was initially denied as “maintenance care,” but after we provided detailed progress notes showing ongoing improvement, the insurer not only paid the original claim but approved additional visits.

Stretch Your Coverage Further All Year Long

Smart calendar planning can dramatically increase your treatment options. Instead of using all your visits in January, spread them strategically throughout the year.

Here’s where Veeva Chiropractic’s comprehensive services become a real advantage: combined therapies can multiply your benefits. Many insurance plans have separate allowances for chiropractic care, acupuncture, naturopathic medicine, and massage therapy.

Deductible timing requires a bit of strategy, especially if you have a high-deductible health plan. If you know you’ll need ongoing care and have other medical expenses coming up, timing everything together can help you meet your deductible faster.

The key to maximizing your benefits is thinking of them as a yearly budget rather than a per-visit expense. Plan ahead, communicate with your healthcare providers about your coverage, and don’t be afraid to ask questions.

Special Scenarios Where Coverage Rules Change

Not all chiropractic care falls under regular health insurance. Certain situations have their own coverage rules and often provide more generous benefits.

Workplace injuries fall under workers’ compensation, which typically covers 100% of medically necessary treatment. Auto accidents trigger Personal Injury Protection (PIP) benefits in many states, including Oregon. Student plans like Studentcare often have specific limits. Federal employees have access to special programs with different coverage rules.

Workplace & Auto Injury Claims: Who Pays First?

When you’re injured at work or in a car accident, special insurance programs often provide much better benefits than your regular health plan.

Priority of payment rules:

1. Workers’ compensation pays first for work-related injuries

2. Auto insurance PIP pays first for car accident injuries

3. Regular health insurance is typically secondary

Important note: You usually can’t choose which insurance to use. If your injury qualifies for workers’ comp or auto insurance, you must use those benefits first. The good news is these programs often provide more comprehensive coverage.

At Veeva Chiropractic, we specialize in auto accident and workplace injury treatment. PIP Chiropractor services ensure you get the care you need while maximizing your available benefits.

Students, Veterans, & Federal Populations

Special populations often have unique insurance benefits that are more generous than typical private plans.

Student coverage examples:

– University of Toronto students get up to $30 per visit for 20 visits annually

– Many student plans include one X-ray per year

Veterans Affairs Canada (VAC) benefits:

– Up to 20 chiropractic sessions per year for eligible veterans

– Additional sessions possible with medical authorization

RCMP members enjoy generous benefits:

– Combined allowance of $4,800 per year for chiropractic, massage, acupuncture, and physiotherapy

– No pre-authorization required within the annual limit

Frequently Asked Questions About How to Get Insurance to Pay for Chiropractic Care

These are the questions we hear most often at Veeva Chiropractic. Let’s clear up the confusion once and for all.

Do I need a referral or pre-authorization for chiropractic visits?

In Oregon, chiropractors are recognized as primary care providers, which means you can usually walk right into our Beaverton, Happy Valley, Hillsboro, or Gresham clinics without stopping at your family doctor first.

But even though Oregon law says you don’t need a referral medically, your insurance plan might still require one for coverage purposes. It’s one of those quirky insurance rules that doesn’t always make medical sense.

Your plan is more likely to require a referral if you have an HMO-style plan, you’re seeking specialized treatments beyond basic adjustments, or your plan lists chiropractic under “specialist care.”

Our staff at Veeva Chiropractic can quickly check what your specific plan requires and help with any necessary paperwork.

What documents are mandatory for a successful chiropractic claim?

Insurance companies are sticklers for paperwork, but once you understand what they want, how to get insurance to pay for chiropractic care becomes much more predictable.

Every successful claim needs the basics: a completed claim form with accurate information, a detailed receipt showing the date of service and treatment provided, plus diagnostic codes (ICD-10) that explain your condition and procedure codes (CPT) that describe the treatment.

Many plans also want to see a treatment plan outlining your care goals and expected duration, along with progress notes showing how you’re responding to treatment.

At Veeva Chiropractic, we maintain comprehensive electronic health records that include all the documentation insurers typically request. Most of the paperwork happens behind the scenes, and you can focus on getting better.

How many chiropractic visits does insurance usually cover each year?

This is probably the question we get asked most often. Most plans fall into pretty predictable patterns once you know what to look for.

Basic workplace plans typically cover 8 to 12 visits per year, while standard benefits packages usually bump that up to 15 to 20 visits annually. Comprehensive coverage might see 25 to 30 visits covered.

Many plans also set dollar limits alongside visit limits. We commonly see annual maximums of $500 to $1,000 for chiropractic care. Since visits typically cost $40 to $80 each, this usually translates to about 10 to 20 visits.

Special circumstances can change everything. Acute injuries often get additional visits approved beyond your normal limits. Work-related injuries through workers’ compensation usually have no visit restrictions at all.

Our advice? Keep track of your visits throughout the year. At Veeva Chiropractic, we help you monitor your benefits usage so there are no unpleasant surprises.

Conclusion

You’ve now got the complete roadmap for how to get insurance to pay for chiropractic care—and it’s not as scary as it seemed at first. Insurance companies love their paperwork and mysterious codes, but once you understand their language, you can speak it fluently.

The most important thing to remember is that taking proactive steps before your first visit sets you up for success. When you verify your benefits, confirm your chiropractor is in-network, and understand your co-payments upfront, you avoid those dreaded surprise bills.

Keeping good records and staying organized makes all the difference. At Veeva Chiropractic, we’ve seen patients save thousands of dollars simply by tracking their visits, submitting claims promptly, and not giving up when a claim gets denied.

Special situations like auto accidents or workplace injuries often provide much better coverage than regular health insurance. If you’re hurt in a car accident or injure your back at work, don’t automatically assume you’ll be paying out-of-pocket.

The statistics don’t lie—nearly 70% of Canadians have extended health coverage that includes chiropractic care, and 4 out of 5 chiropractic patients successfully use their insurance benefits.

At Veeva Chiropractic, we’re not just here to treat your back pain, neck stiffness, or injury recovery—we’re here to help you steer every aspect of your healthcare journey. Our experienced team across our Beaverton, Happy Valley, Hillsboro, and Gresham locations has helped thousands of patients maximize their insurance benefits while focusing on what really matters: getting you back to pain-free living.

If you’re recovering from an accident, more info about accident recovery services can help you understand your specialized coverage options.

Veeva Chiropractic is here to guide you on every step toward pain-free living and fully covered care. We know that dealing with insurance shouldn’t add stress to your recovery process. That’s why our team is always ready to help verify your benefits, submit your claims, and even assist with appeals when necessary. Contact us today, and let’s work together to get you the care you deserve—with your insurance picking up the tab.