Is Your Back Covered? Understanding Insurance for Chiropractic Care

Is Insurance Coverage for Chiropractic Care Complicated? Not Anymore

Does insurance cover chiropractic care? Yes, most health insurance plans provide some coverage for chiropractic services, but with specific limitations. Here’s a quick overview:

| Insurance Type | Typically Covers Chiropractic? | Common Limitations |

|---|---|---|

| Private/Employer Plans | Yes (87% of plans) | Visit limits, referral requirements, in-network only |

| Medicare Part B | Yes | Only spinal manipulation for subluxation, 20% coinsurance |

| Medicaid | Varies by state | Limited services, strict medical necessity |

| Workers’ Compensation | Yes (all 50 states) | Must be work-related injury |

| Auto Insurance (PIP) | Yes | Must be accident-related, time limits apply |

| VA/Military | Yes | Available at 60+ facilities |

When your back is acting up and the pain won’t quit, chiropractic care might be the answer. But before you schedule that first adjustment, you’re probably wondering about the cost and if your insurance will help pick up the tab.

You’re not alone. Over 35 million Americans seek chiropractic treatment each year, and many face confusion about their coverage.

The truth is that insurance coverage for chiropractic care exists but varies widely. Most major health plans cover basic spinal adjustments when deemed medically necessary. However, they often impose restrictions like:

- Requiring doctor referrals

- Limiting the number of visits (typically 10-30 per year)

- Covering only specific services while excluding others

- Requiring you to see in-network providers

At Veeva Chiropractic, we understand navigating insurance can be as painful as the back problems bringing you in. That’s why we’ve created this comprehensive guide to help you understand your benefits before your first crack.

What Is Chiropractic Care & Who Can It Help?

Chiropractic care is a gentle, hands-on approach to healthcare that focuses on your body’s musculoskeletal system—particularly your spine. Instead of medications or surgery, chiropractors use skilled manual adjustments to improve alignment, ease pain, and help your body heal naturally.

Behind every adjustment is a highly trained professional. Chiropractors don’t just hang a shingle after a weekend course—they complete intensive education including undergraduate studies (usually with pre-med courses), followed by a four-year Doctor of Chiropractic (D.C.) program. That’s over 4,200 hours of classroom, lab, and hands-on clinical training before they ever treat their first patient. Plus, they must pass rigorous national board exams and maintain their state license through ongoing education.

You might be surprised by the range of conditions chiropractic care can address. While back pain and neck pain bring many patients through the door initially, chiropractors regularly help with headaches, sciatica, joint pain in arms and legs, sports injuries, workplace incidents, car accident recovery, and even poor posture.

Chiropractic care isn’t just for adults with existing pain, either. Pregnant women often find relief from pregnancy-related discomfort through specialized prenatal techniques that maintain proper pelvic alignment and can contribute to smoother deliveries. For the littlest patients, pediatric chiropractic uses extremely gentle approaches (nothing like the “cracks” you might imagine) to address issues like colic, ear infections, and developmental concerns. Many wellness-focused individuals without specific pain also benefit from maintenance adjustments that optimize nervous system function and prevent future problems.

Don’t just take our word for it—research published in JAMA has shown that spinal manipulation can effectively treat acute low back pain, with many patients reporting significant improvements in their overall function and quality of life.

First Visit & Follow-Up Expectations

Your first chiropractic visit is like meeting a new friend who happens to be a spine detective. It’s more comprehensive than follow-ups and typically includes:

A thorough health history where you’ll share your current symptoms, past injuries, medical conditions, and lifestyle factors. Your chiropractor will then perform physical, neurological, and orthopedic tests to assess your posture, range of motion, and problem areas.

Sometimes, X-rays or other imaging might be needed to get a clearer picture of what’s happening inside. Based on all these findings, your chiropractor will explain your diagnosis and recommend a personalized treatment plan, including how often you should come in and for how long. If appropriate, you might receive your first adjustment during this initial visit.

Follow-up visits move more efficiently. Your chiropractor will briefly check your progress, perform specific adjustments based on your treatment plan, possibly include complementary therapies like electric stimulation or soft tissue work, and send you home with exercises or stretches to support your care.

A little soreness after your first few adjustments is completely normal—similar to how your muscles might feel after trying a new workout. This typically fades within 24-48 hours as your body adapts to its improved alignment.

Active Treatment vs. Maintenance Care

When it comes to the question “does insurance cover chiropractic care?“, understanding the difference between active treatment and maintenance care is crucial.

Active treatment addresses specific problems like that shooting pain down your leg or the neck stiffness that won’t quit. It’s designed to correct identifiable issues, show measurable improvement, and typically ends once you’ve reached maximum improvement. This type of care is what insurance companies generally cover when it’s deemed medically necessary.

Maintenance care (sometimes called wellness or preventive care) is more like regular oil changes for your spine. It’s designed to maintain the improvements you’ve achieved and prevent future problems. These visits typically happen less frequently—maybe monthly or quarterly—and unfortunately, most insurance plans don’t cover them.

Insurance carriers draw this line because they’re primarily concerned with treating active problems, not preventing future ones. Once your provider notes you’ve reached “maximum medical improvement,” continued care often gets classified as maintenance and no longer qualifies for coverage.

Understanding these distinctions helps you prepare financially for your care journey and avoid unexpected bills. While insurance might not cover every aspect of chiropractic care, many patients find the investment in their long-term spinal health well worth the out-of-pocket expense for maintenance visits.

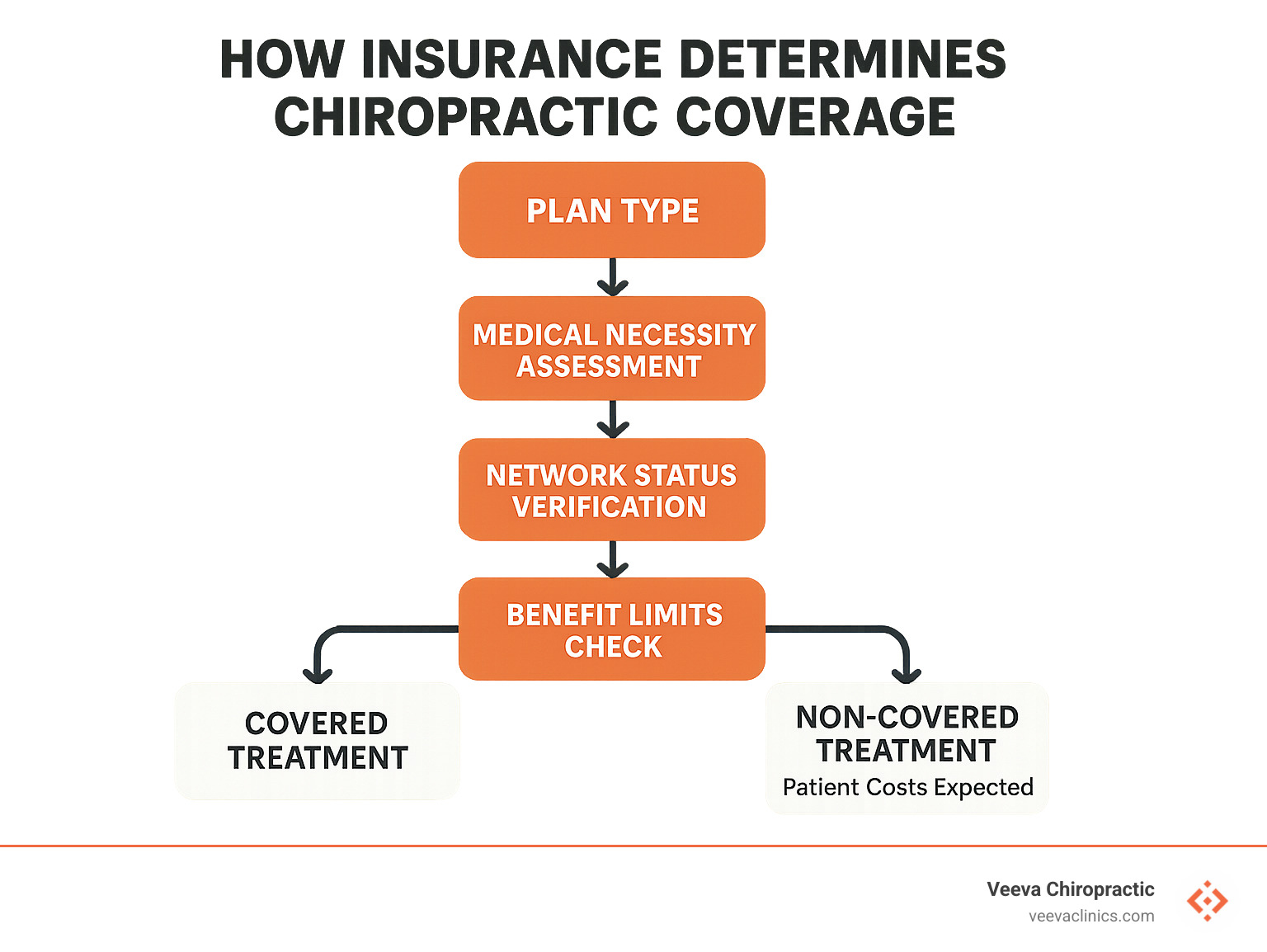

Does Insurance Cover Chiropractic Care?

Yes, most insurance plans do cover chiropractic care—but there’s more to the story. While about 87% of insured American workers have some form of chiropractic coverage in their health plans, what that actually means for your wallet varies quite a bit.

Here’s something many people don’t realize: under the Affordable Care Act (ACA), chiropractic care isn’t considered an “essential health benefit” that plans must cover. Instead, it falls into the “nice to have but optional” category. This means your coverage depends on:

- Your specific insurance plan’s details

- Where you live (some states require certain plans to include chiropractic benefits)

- Your employer’s choices when selecting healthcare options

Most insurance plans that do cover chiropractic care come with some strings attached. You might face visit limits (typically 10-30 per year), need a referral from your primary doctor, or have to prove the treatment is medically necessary rather than preventive. Your insurance will also likely require proper documentation showing your progress, and many plans only cover providers within their network.

The good news? The trend toward chiropractic coverage has been improving. Between 2012 and 2017, the percentage of U.S. adults using chiropractic services increased from 9.1% to 10.3%. More insurers are recognizing that chiropractic care offers a cost-effective alternative to surgery and medication for many conditions.

Private & Employer-Sponsored Plans – does insurance cover chiropractic care

Private and employer-sponsored health plans typically offer the most comprehensive chiropractic coverage, though benefits vary significantly depending on your plan type.

If you have an HMO (Health Maintenance Organization) plan, you’ll likely need a referral from your primary care doctor before seeing a chiropractor. These plans typically limit you to in-network providers only, may have stricter visit limits, and often require pre-authorization if you need extended treatment.

PPO (Preferred Provider Organization) plans generally give you more flexibility. You can usually choose any chiropractor, though you’ll pay less with in-network providers (typically paying just a copay) compared to out-of-network ones (where you might cover 30-50% of the cost). PPOs also tend to allow more visits annually.

If you have a High-Deductible Health Plan with an HSA, you’ll need to meet your deductible before coverage kicks in. The silver lining? You can use your tax-advantaged HSA funds to pay for chiropractic care even when it’s not covered by insurance. After meeting your deductible, coverage often resembles what you’d get with a PPO.

When checking your private insurance coverage for chiropractic care, pay special attention to the difference between in-network and out-of-network benefits—this can dramatically impact your costs. An in-network visit might mean a simple $25 copay, while going out-of-network could leave you paying half the bill after meeting your deductible. Also check for any pre-authorization requirements, annual visit or dollar amount caps, and which specific services are covered beyond basic spinal adjustments.

Does insurance cover chiropractic care under private plans? Generally yes for medically necessary treatment, but the details matter enormously.

Medicare & Medicaid Rules – does insurance cover chiropractic care

Medicare Coverage:

Medicare’s approach to chiropractic care is straightforward but limited. Under Medicare Part B:

- Coverage is restricted to manual manipulation of the spine to correct a subluxation (when spinal bones move out of position)

- The subluxation must be documented by a qualified provider

- Medicare pays 80% of the approved amount after you meet your Part B deductible

- Medicare does NOT cover other chiropractic services like X-rays, massage therapy, acupuncture, or preventive maintenance care

According to Medicare’s official coverage information, your treatment must be deemed medically necessary with proper documentation. If your chiropractor recommends care beyond what Medicare considers reasonable for your condition, those claims may be denied.

It’s worth noting that Medicare Advantage (Part C) plans sometimes offer additional chiropractic benefits beyond what Original Medicare provides, so check your specific plan details if you have this type of coverage.

Medicaid Coverage:

When it comes to Medicaid and chiropractic care, your coverage largely depends on which state you call home:

- Some states offer robust coverage similar to private insurance

- Others limit services to specific conditions or patient populations

- Some states don’t cover chiropractic care at all

Here in Oregon, the Oregon Health Plan (Medicaid) currently covers chiropractic services for certain qualifying conditions, but coverage is limited and typically requires prior authorization.

If you’re covered by Medicaid, we recommend contacting your specific plan administrator before scheduling care to verify your chiropractic benefits.

Workers’ Comp, Auto PIP & VA / Military Benefits

Workers’ Compensation:

If you’ve been injured on the job, here’s good news: all 50 states include chiropractic care in their workers’ compensation programs. This coverage is typically comprehensive, covering 100% of your treatment costs as long as:

- Your injury is clearly work-related

- Your care is properly documented and authorized

- Your treatment is showing measurable progress

- You’re following your prescribed care plan

In Oregon specifically, workers’ compensation cases often include chiropractic care as part of managed care organizations (MCOs) that coordinate treatment for injured workers.

Auto Insurance (Personal Injury Protection):

Been in a car accident? Chiropractic care is generally covered under Personal Injury Protection (PIP) insurance. Here in Oregon, PIP is mandatory and typically covers:

- “Reasonable and necessary” medical expenses, including chiropractic treatments

- Care received within two years of your accident date

- Services regardless of who was at fault

PIP coverage is often more generous than regular health insurance when it comes to chiropractic care, typically allowing more visits and covering a wider range of services.

VA and Military Benefits:

Veterans and active military personnel can access chiropractic care through several channels:

- VA medical facilities (now available at more than 60 locations)

- Military treatment facilities on more than 60 bases

- TRICARE coverage for active duty members and their families

The VA has been expanding its chiropractic services in recent years as part of a broader commitment to offering non-drug approaches to pain management.

For all these specialized insurance types, proper documentation is absolutely crucial. Your chiropractor must clearly establish the connection between your injury and treatment, demonstrate medical necessity, and show your progress through objective measures.

Decoding Costs: Deductibles, Copays & Networks

Let’s face it – the financial side of healthcare can sometimes feel like deciphering a foreign language. Understanding what you’ll actually pay for chiropractic care before you walk in the door can save you from that sinking feeling when the bill arrives.

Think of your insurance plan as a puzzle with several important pieces that fit together to determine your costs:

Deductible is the amount you need to pay out-of-pocket before your insurance kicks in. If your deductible is $1,500, you’ll be covering the full cost of your chiropractic visits until you’ve spent that amount on eligible healthcare throughout the year.

Copay works like an admission ticket – it’s the fixed amount (usually $20-35) you pay each time you visit your chiropractor. You’ll typically hand this over at the front desk before your appointment.

Coinsurance is your share of the cost-splitting arrangement with your insurance after you’ve met your deductible. With 20% coinsurance, you’re responsible for 20% of the allowed charges while your insurance handles the remaining 80%.

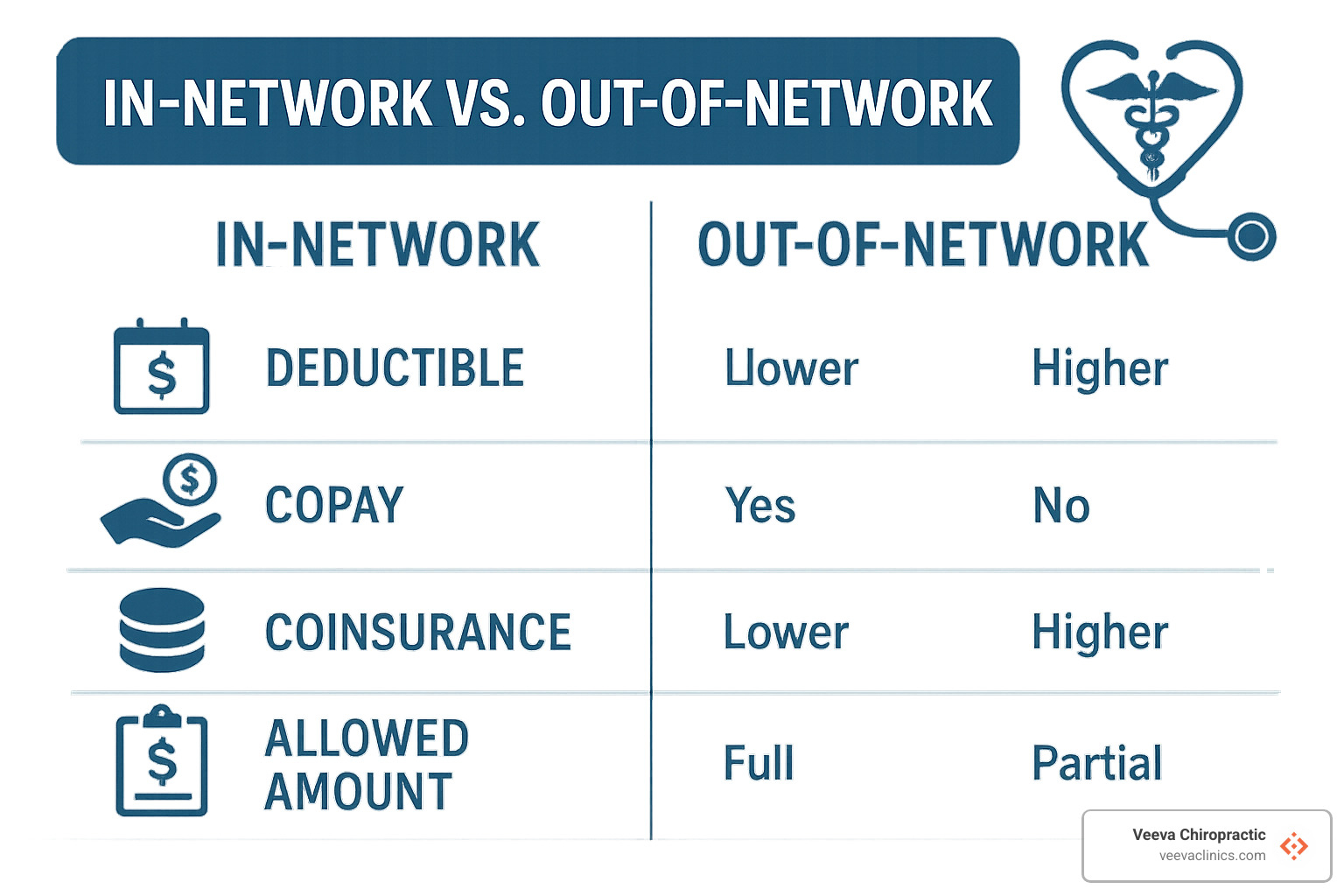

Allowed Amount is the maximum your insurance considers reasonable for a service. This is crucial because if your chiropractor charges more than this amount, you might be on the hook for the difference – unless they’re in your network.

Network Status is perhaps the biggest factor affecting what comes out of your wallet. When a chiropractor is “in-network,” they’ve agreed to accept your insurance company’s allowed amounts as payment in full (minus your share).

Here’s how network status affects what you’ll pay:

| Cost Factor | In-Network Provider | Out-of-Network Provider |

|---|---|---|

| Deductible | Usually lower | Often higher (separate from in-network) |

| Copay/Coinsurance | Lower (typically $20-35 copay) | Higher (often 40-50% coinsurance) |

| Balance Billing | Not allowed | Allowed (you pay the difference) |

| Paperwork | Provider handles claims | You may need to submit claims |

| Pre-authorization | Often handled by provider | May be your responsibility |

Sometimes, insurance companies add another player to the game – Third-Party Administrators (TPAs) like American Specialty Health (ASH). These companies manage chiropractic benefits on behalf of your insurer and may have their own networks and rules that differ from your primary insurance.

After each visit, you’ll receive an Explanation of Benefits (EOB) from your insurance company. This isn’t a bill – it’s more like a receipt explaining what services were provided, what insurance paid, and what you might owe. Think of it as the “show your work” part of the insurance math problem.

How Many Visits Are Covered & When Do Benefits Reset?

Most insurance plans won’t give you a blank check for unlimited chiropractic visits. Instead, they set boundaries in one of two ways:

Annual Visit Caps work just like they sound – you get a specific number of covered visits (usually 20-30) per calendar year. Once you’ve used them all, any additional treatment comes straight from your pocket until your benefits reset (typically January 1st).

Rolling Limits are a bit trickier – instead of a calendar year, these limits are based on your specific condition or treatment period. For example, you might get 12 visits per “episode of care” or within a 90-day window.

Even with these limits, many insurers want to check in after you’ve had 6-12 visits through what’s called a Medical Review Threshold. This is where they evaluate whether continued care is actually helping you improve.

To get the most from your benefits:

Be strategic with scheduling, especially near year-end if you’ve already met your deductible. Those December visits might be much cheaper than waiting until January when your deductible resets.

Keep track of how many visits you’ve used – hitting your limit unexpectedly can turn what you thought was a $25 copay visit into a $100+ out-of-pocket expense.

Your chiropractor can sometimes request additional visits beyond your limit by showing you’re making progress but still need care. This is where detailed progress notes become your best friend.

Insurance companies expect to see improvement. Your chiropractor should document objective measures like increased range of motion or decreased pain scores to justify continued treatment.

Billing Process & What the EOB Really Means

When you receive that Explanation of Benefits after your visit, it can look like a confusing jumble of codes and numbers. Here’s what’s happening behind the scenes:

Your chiropractor uses specific CPT Codes (Current Procedural Terminology) to tell your insurance exactly what services you received. Common chiropractic codes include:

* 98940 for adjustments to 1-2 spinal regions

* 98941 for adjustments to 3-4 regions

* 98942 for adjustments to all 5 spinal regions

* 99202-99205 for new patient evaluations

* 99211-99215 for established patient visits

These codes, along with diagnosis codes that explain why you needed care, get submitted to your insurance company, which then determines:

* If your plan covers these services

* If they’re medically necessary based on your diagnosis

* What the “allowed amount” is for each service

* How much they’ll pay versus what you’re responsible for

Your EOB breaks all this down, often using explanation codes for any services they’re not covering. If something gets denied, it’s usually for one of these reasons:

The service isn’t covered under your plan (like maintenance care or certain therapies).

Medical necessity wasn’t established – meaning your diagnosis didn’t justify the treatment in their eyes.

You’ve exceeded your visit limit for the year or treatment period.

Information is missing or incorrect on the claim form.

Duplicate billing occurred (same service billed twice).

If you receive a denial you believe is incorrect, don’t just accept it! You have the right to appeal, and your chiropractor’s billing staff can often help by providing additional documentation or correcting errors.

At Veeva Chiropractic, we understand that dealing with insurance can sometimes be as painful as the back problems bringing you in. Our staff is always ready to help you steer these complexities so you can focus on what matters most – feeling better.

Maximizing Benefits & Paying If Coverage Runs Out

Getting the most from your chiropractic insurance doesn’t have to be complicated. With a little preparation and know-how, you can stretch those benefits further and find affordable options when coverage ends.

Before your spine gets its first adjustment, take time to understand exactly what your insurance covers. Call your insurance company directly or check your online portal to verify your chiropractic benefits. Find out if your preferred chiropractor is in-network, how many visits you’re allowed annually, and whether you need a referral from your primary doctor. This simple step can save you hundreds of dollars and prevent billing surprises down the road.

Don’t forget about those tax-advantaged accounts sitting in your financial toolbox. HSAs (Health Savings Accounts), FSAs (Flexible Spending Accounts), and HRAs (Health Reimbursement Arrangements) let you pay for chiropractic care with pre-tax dollars. That’s like getting an automatic discount equal to your tax bracket on every adjustment! Even if your insurance denies coverage, these accounts can make treatment more affordable.

Some patients find value in supplemental coverage specifically designed for alternative therapies. These specialized plans can fill the gaps left by traditional insurance. Discount programs and membership plans can also reduce your out-of-pocket costs, while accident policies might cover chiropractic care if you’re injured.

When your insurance benefits run out but your back still needs attention, don’t worry – you have options. Many chiropractors offer cash discounts of 20-30% off their standard rates. Ask about package deals for multiple visits, which often come with significant savings. Most practices are happy to discuss payment plans that spread costs over time, making continued care more manageable for your budget.

At Veeva Chiropractic, we believe financial concerns shouldn’t stand between you and the care you need. We’re committed to helping patients understand their cost breakdown for chiropractic care and finding solutions that fit their unique financial situations.

Steps to Verify Coverage & Find an In-Network Chiropractor

Finding a great chiropractor who accepts your insurance doesn’t have to be a pain in the neck. Here’s how to do it right:

Start with your policy documents – dig out your Summary of Benefits and Coverage (SBC) and look under “Specialist visits” or “Alternative care.” These sections will outline your chiropractic benefits and any limitations. If the insurance-speak feels overwhelming, don’t worry – that’s normal!

Your next step is reaching out directly to your insurance company. Call the member services number on your card and ask specifically about chiropractic coverage. Be direct: “Does insurance cover chiropractic care under my specific plan?” Then drill down into the details – visit limits, referral requirements, and what your copay will be.

Most insurance companies now offer online provider directories that make finding in-network chiropractors much easier. Filter your search by location and specialty to narrow down your options. These directories can sometimes be outdated, so always verify a provider’s network status before your first visit.

When speaking with insurers or potential providers, ask pointed questions: “Is Dr. Smith in-network for my specific plan?” “What will my out-of-pocket cost be per visit?” “Do I need pre-authorization?” “Which chiropractic procedure codes (CPT codes) are covered?” The answers will help you avoid unexpected bills.

Always get confirmation in writing when possible. Request an email summary of your benefits, save screenshots from your insurer’s website, and keep detailed notes from phone conversations (including representative names and reference numbers). This documentation can be invaluable if billing issues arise later.

Finally, double-check everything with the chiropractic office before your first appointment. Ask if they regularly work with your insurance plan and their experience with claim approvals. A good chiropractic office will help verify your benefits before treatment begins.

Smart Alternatives When Insurance Says “No”

When your insurance denies coverage but your spine is still crying out for help, it’s time to get creative. Fortunately, there are several ways to make chiropractic care more affordable without insurance.

Cash rates can offer surprising savings. Many chiropractors provide significant discounts (typically 20-40% off) for patients who pay at the time of service. These reduced rates acknowledge the office’s savings on billing paperwork and claim submissions. Don’t be shy about asking for the best possible cash price – most practices are happy to discuss their options.

Care packages can dramatically lower your per-visit cost. Many chiropractors offer prepaid treatment packages that bring the per-visit price down considerably. Just make sure any package includes a reasonable refund policy if you can’t use all your visits. Be cautious about very long-term commitments – a good package should offer savings without locking you into years of care.

Even if your chiropractor is out-of-network, you might still get some money back from your insurance. Ask for a detailed receipt called a Superbill after each visit, which you can submit to your insurance for possible partial reimbursement. This works especially well with PPO plans that offer out-of-network benefits.

Don’t overlook community resources. Chiropractic schools often run teaching clinics where supervised students provide care at substantially reduced rates. Community health centers sometimes include chiropractic services on their sliding fee scales. Some private practitioners also offer income-based fee reductions for patients in need.

If you’re seeing multiple providers – perhaps a chiropractor, massage therapist, and physical therapist – ask about bundled service discounts. Integrated practices like Veeva Chiropractic can often create comprehensive care plans that maximize value by combining different therapies efficiently.

Finally, work with your chiropractor to develop a robust home exercise program. With the right self-care routine, you might be able to space out professional visits while maintaining progress. Investing in recommended self-care tools (like foam rollers or therapeutic pillows) can extend the benefits of in-office treatments.

Remember to weigh the cost against potential benefits. Sometimes paying out-of-pocket for effective chiropractic treatment is more economical than continuing to suffer or pursuing more expensive interventions like surgery or long-term medication.

Frequently Asked Questions About Chiropractic Insurance

Let’s tackle some of the most common questions we hear from patients about chiropractic insurance. I’ve gathered these from hundreds of conversations with people just like you who are trying to make sense of their coverage options.

Does insurance cover chiropractic care for wellness visits?

Generally no. This is one of the most disappointing answers I have to give patients who are proactive about their health. Most insurance plans only cover chiropractic care that checks these three boxes:

- It must be medically necessary to treat a specific, documented condition

- Your provider needs to expect significant improvement from the treatment

- Your progress must be tracked with objective measurements

Insurance companies typically draw a clear line between “active treatment” (fixing a problem) and “maintenance care” (preventing future problems). While both have value, they usually only pay for the former.

If you’re interested in wellness visits, don’t despair! Many patients find that periodic maintenance adjustments are worth paying for out-of-pocket because they help prevent more serious (and expensive) problems down the road. Some employers also offer wellness programs or HSA/FSA funds that can offset these costs.

How much does a chiropractic visit cost without insurance?

When patients ask me this question, I always wish I could give a simple answer. The truth is, costs vary quite a bit depending on several factors.

For a typical cash-paying patient, you can expect to invest:

* $100-200 for an initial evaluation (which is more comprehensive)

* $30-100 for a standard adjustment visit

* $10-50 for additional therapies like electric stimulation or ultrasound

These ranges reflect differences based on your location (city practices generally charge more than rural ones), your chiropractor’s experience level, and the complexity of your condition. In Portland and surrounding areas like Beaverton and Hillsboro, prices tend to fall in the middle of these ranges.

The good news? Many chiropractors (including us at Veeva) offer package deals or membership options that can bring your per-visit cost down significantly. It never hurts to ask!

What should I watch for in prepaid treatment plans?

While prepaid plans can offer real savings, I’ve unfortunately seen some practices use them in ways that don’t serve patients well. Here’s my honest advice on what to watch for:

Be wary of high-pressure sales tactics. Your first visit should be about understanding your condition, not signing up for a year of care. A good chiropractor will give you time to think about their recommendations and won’t make you feel rushed into a decision.

Question excessive visit recommendations. Most acute conditions show measurable improvement within 6-12 visits. If someone’s recommending 40+ visits right off the bat without clear benchmarks for progress, that’s a red flag.

Check the refund policy carefully. Life happens—you might move, change jobs, or find the treatment isn’t helping as expected. Make sure you understand what happens to your investment if you need to discontinue care.

Look for clear progress measures. Your treatment plan should include regular reassessments and objective ways to track improvement. Without these, how will you know if the care is working?

At Veeva Chiropractic, we believe in transparent recommendations based on what we’re actually seeing in your body, not on filling appointment slots. We’ll never suggest more care than we genuinely believe will help your condition.

If you’re still unsure about how insurance might cover your specific chiropractic needs, our front desk team is happy to help verify your benefits before your first visit. Just give us a call—we speak insurance jargon so you don’t have to!

Conclusion & Next Steps

Feeling a bit more confident about your chiropractic insurance coverage now? Throughout this guide, we’ve unwrapped the sometimes confusing world of insurance and made it clearer for you.

The good news is that most insurance plans do cover chiropractic care – but as we’ve seen, they come with their own set of rules and limitations. Your coverage typically extends to care that’s deemed medically necessary for active conditions, but rarely covers those wellness visits that keep you feeling great long-term.

Whether you’ll be paying $25 or $80 per visit largely depends on whether your chiropractor is in-network, and how many visits you have left in your annual allowance. These are the details worth knowing before your spine gets its first adjustment!

Remember these five simple steps to make the most of your coverage:

First, verify before you visit. A quick call to your insurance company can save you from unexpected bills later. Ask specifically about chiropractic benefits and get the details in writing if possible.

Second, understand what’s covered versus what’s not. That active treatment for your throbbing back pain? Likely covered. Those monthly tune-ups to keep you feeling great? Probably coming out of your pocket.

Third, keep track of your visits. Insurance plans typically cap the number of chiropractic sessions they’ll cover annually. Knowing where you stand helps avoid surprise bills.

Fourth, review all your paperwork. Those Explanations of Benefits aren’t just paper clutter – they tell you exactly what your insurance paid and why.

Fifth, talk openly with your chiropractor about costs. Most care teams are happy to help you understand what you’ll owe and find solutions that fit your budget.

Here at Veeva Chiropractic, we believe your financial concerns shouldn’t keep you from getting the care you need. Our friendly team works with patients across our Oregon locations – Beaverton, Happy Valley, Hillsboro, and Gresham – to steer insurance complexities and find affordable options for everyone.

Whether you’re nursing a persistent backache, recovering from a fender bender, or dealing with a workplace injury, we’ve got your back (literally!). We work with most major insurance plans, accept workers’ compensation and auto insurance claims, and offer reasonable self-pay rates for those times when insurance just won’t cooperate.

Curious if your plan will cover the care you need? Reach out today, and our staff will happily check your benefits before you even schedule that first visit.

For more information about our comprehensive chiropractic services, visit our website or give any of our convenient Oregon locations a call.

Your journey to feeling better begins with understanding your coverage—and we’re here to make that process as smooth and pain-free as your spine will soon be!